Goods and Services Tax or GST is a broad-based consumption tax levied on the import of goods (collected by Singapore Customs), as well as nearly all supplies of goods and services in Singapore. In other countries, GST is known as the Value-Added Tax or VAT.

GST exemptions apply to the provision of most financial services, the supply of digital payment tokens, the sale and lease of residential properties, and the importation and local supply of investment precious metals. Goods that are exported and international services are zero-rated.

On this page:Most local sales fall under this category.

E.g. sale of TV set in a Singapore retail shop

Sale of imported low-value goods (from 1 Jan 2023)

E.g. Sale of tennis racquet by overseas online merchant to customer in Singapore at $330, excluding freight and insurance

Imported Services

E.g. Procurement of marketing services from overseas service provider

Financial services

E.g. issue of a debt security

As a business, you must register for GST when your taxable turnover exceeds $1 million.

You may also be liable for GST registration under the Reverse Charge and Overseas Vendor Registration regimes. For more information, please refer to the section on Reverse Charge and Overseas Vendor Registration.

If your business taxable turnover does not exceed $1 million, you may still choose to voluntarily register for GST after careful consideration.

Only GST-registered businesses can charge and claim GST from their effective date of GST registration. Non-GST registered businesses are not allowed to charge or claim GST.

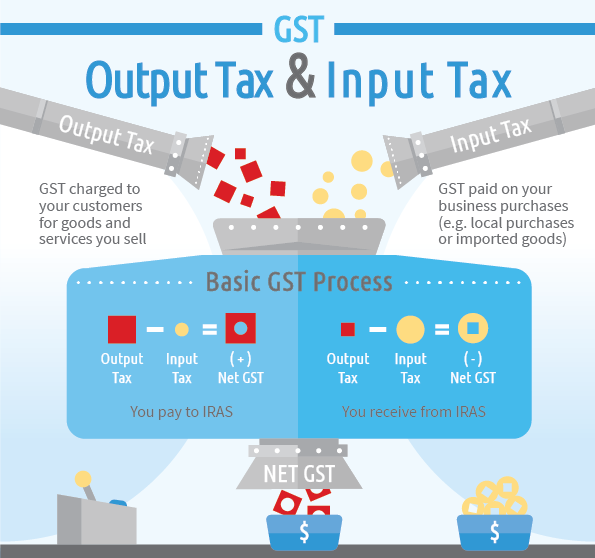

If you are registered for GST, you must charge GST on all taxable supplies at the prevailing GST rate, except for supplies that are subject to customer accounting. The GST that you charge and collect is known as output tax. Output tax must be paid to IRAS within a month from the end of the accounting period. Refer to our page on filing and payment due dates for more information.

If you have wrongfully charged or collected GST, you must remit the GST wrongly collected to IRAS.An exception where a non-GST registered person is required to charge and account for GST is when it sells or rents out a GST-registered business assets in satisfaction of a debt owed. This applies to non-GST registered third parties, such as mortgagees, financiers and auctioneers. For details on how to account for GST in such scenario, please refer to our page on selling/ renting out asset in satisfaction of debt.

If you are registered for GST, you can claim the GST incurred on business purchases (including imports) and expenses, as input tax in your GST return. This is subject to you fulfilling the conditions for claiming input tax.

There are exceptions where non-GST registered businesses in specific industries are given concessions (subject to conditions) by the Minister to claim the GST incurred. These exceptions are:

To claim the GST incurred, qualifying funds, S-REITs and S-RBTs need to submit a quarterly Statement of Claims to IRAS within one month from the end of the respective quarters.

As an administrative concession, funds and trusts may file their quarterly Statement of Claims after the due date, subject to the following conditions:

Period of claims: 1 Apr 2023 to 30 Jun 2023

Qualifying funds, S-REITs and S-RBTs can submit the Statement of Claims latest by 30 Jun 2028.

Additionally, you may be able to claim GST incurred before GST registration or incorporation, provided that you fulfil certain conditions. For more information, please refer to our page on claiming GST incurred before GST registration/ incorporation.

This input tax credit mechanism ensures the taxation of only the value-add at each stage of a supply chain.

A GST-registered manufacturer imports leather from overseas to manufacture a bag. The manufacturer sells the bag to a GST-registered retailer. Thereafter, the retailer sells the bag to a consumer.

This is how GST works at each stage of the value chain:

Pays GST to Singapore Customs for the import of leather Import value = $100Import GST paid = 9% X $100 = $9 (input tax claimable from IRAS)

Charges and collects GST for sale of bags to retailer Selling price to retailer = $200Pays GST to Retailer

Purchase value = $300

GST paid = 9% X $300 = $27

End consumer is not GST-registered. Therefore, he cannot claim the GST paid on his purchase from IRAS.

GST was introduced in 1 Apr 1994 to enable Singapore to shift its reliance from direct taxes to indirect taxes. GST has also enabled Singapore to sustain a lower income tax rate. Being a tax on consumption, and not income, GST inherently encourages savings and investments.